Roof Depreciation Life Rental Property

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

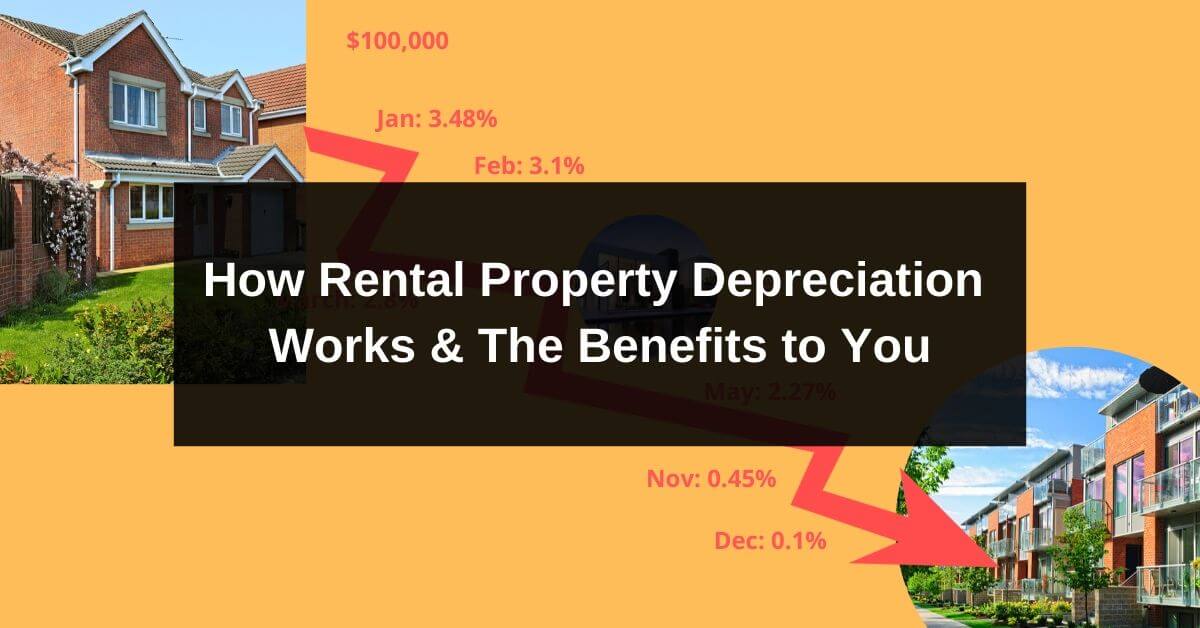

How Rental Property Depreciation Works The Benefits To You

Rental Property Depreciation Rules Schedule Recapture

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

How The New Tax Law Affects Rental Real Estate Owners

Real Estate Investing Frequently Asked Questions Most Common Faqs Real Estate Rentals Renting Out Your House Rental Property

These are the useful lives that the irs deems for both types of properties.

Roof depreciation life rental property.

8 Proven Ways To Feel Safe And Secure With Tenants In Your Own Home Landlording Investment Property For Sale Rental Property Income Property

23 Items For Depreciation On Your Triple Net Lease Property Net Lease Tax Deductions Capital Gains Tax

Why Depreciation Matters For Rental Property Owners At Tax Time Stessa

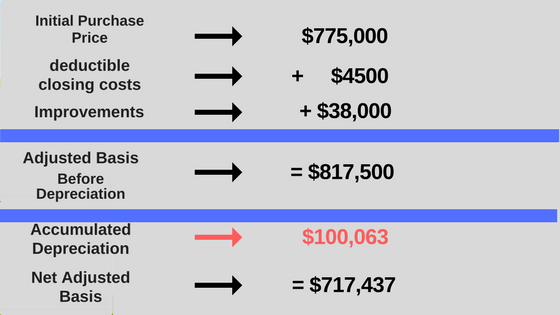

Calculating Your Profit When Selling Your Rental Property Mortgage Blog

Source : pinterest.com